Offerpad Solutions, Inc. operates a real estate platform that enables consumers to seamlessly buy and sell their homes using a mobile device.

Offerpad Solutions de-SPACed on September 2nd with a 92% redemption rate. leaving the float at 3,387,913 shares. As a result, this leaves the stock to trade volatile.

From Reddit u/heshortbig_

Just like IRNT, OPAD’s options can put market makers in the position where they would need to buy over 100% of OPAD’s current float in order to hedge their risk from writing options to retards like you all on WSB – and frankly, it’s not that hard for OPAD to reach the point where this would happen. As further OTM call options become in the money, market makers will have to buy more and more of these shares to sell to you if you decide to exercise the contract. This is because of the options Greeks Delta and Gamma. Now normally I know that for you retards “options Greeks” usually means the options your wife’s Greek boyfriend tells you to buy, but for this play Delta and Gamma are super important.

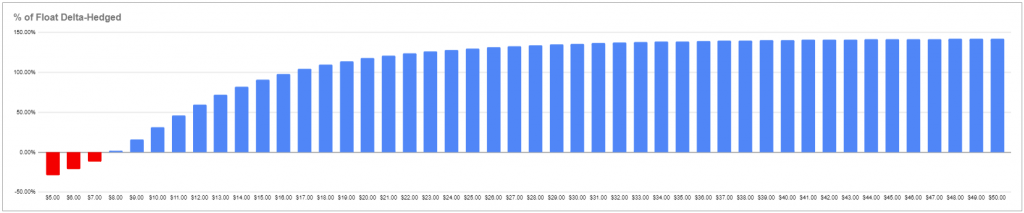

Since I know you dgaf about options Greeks, let me try to dumb it down for you apes with a picture:

Based on the options open interest as of yesterday, if OPAD reached $16 then market makers would need to hedge 98.21% of the current float. At Wednesday’s close price, only 29.72% of the float would need to be hedged – still a huge amount, but clearly this thing has room to run. And on top of that, OPAD already managed to reach $16 last Thursday before it was swatted down by short sellers.

Right now, as the price increases past $16 market makers would need to buy less and less additional stock to hedge since the stock price becomes further and further from the open options interest. If more people buy more OTM options, though, then the price could run even higher because market makers would need to buy even more stock even after the price runs (aka the situation IRNT is in right now). This is delta and gamma at play, and what can create a gamma squeeze. This covering would be incredibly difficult for market makers to do because of the low number of stock available in the float. OPAD already briefly reached $16 last Thursday and OPAD’s options volume and open interest has been steadily increasing, so who knows what the fuck could happen over the next few days as we head into September options expiration.

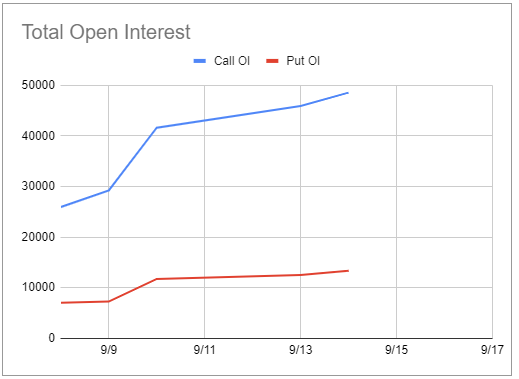

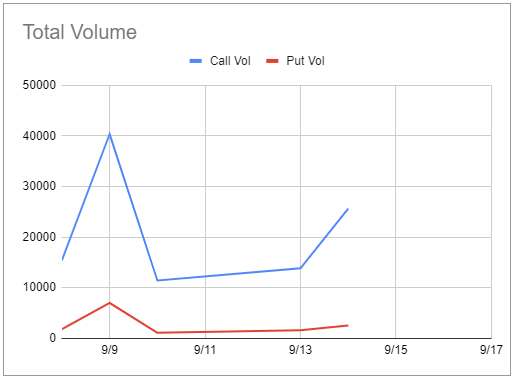

Also, since you’re a degenerate and have likely already started to buy options on this shit before even finishing my DD you may have noticed that OPAD’s options open interest and volume is much lower than IRNT’s. For one, this is probably because you apes haven’t caught wind of OPAD until right now and haven’t yet started buying large amounts of retardedly OTM calls. However, even with the lower overall open interest there is still a ton of potential.

Here is OPAD’s total open interest and volume since I started tracking it last week:

To begin with, even taking out the gamma squeeze considerations with OPAD it’s a retarded idea to short this stock right now. OPAD is a legitimate growth stock with many signs that it’s significantly undervalued right now and could likely be a nice return even if you were to just buy and hold. For example, OPAD’s 2023 projected revenue is $1.7-$1.85 billion. With their current market cap, they would only be trading at a 1.55 multiple; OPAD’s peers are trading at multiple times higher than that. Even if all outstanding warrants are executed and after PIPE unlock, this stock will still be undervalued relative to its peers.

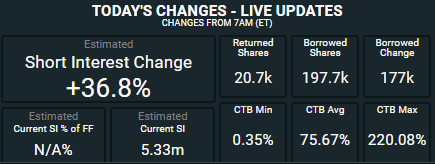

The crazy thing about the shorting is that according to Ortex, short sellers have now managed to accumulate a total short interest of 5.33 million – which is 157% of the current float. Short interest increased 36% yesterday, cost to borrow reached as high as 220.08%, and utilization is at 99.98% (aka there are pretty much no shares left to short).